Overview

Indiana has unique county tax rules that impact payroll calculations for employees based on their residence and work location on January 1st of each year. CMiC has implemented special configurations to support these tax regulations, ensuring accurate tax calculations for employees working or residing in Indiana.

This

Indiana County Tax Setup in CMiC

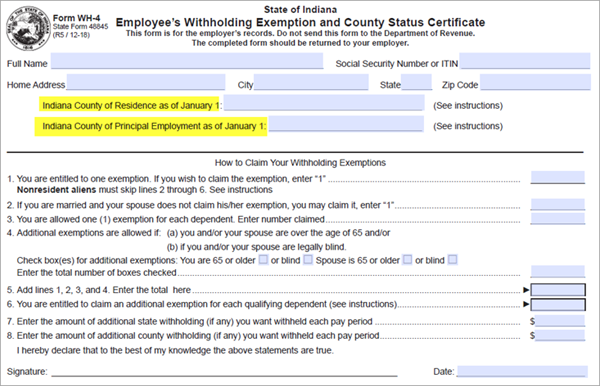

Form WH-4: State of Indiana Employee's Withholding Exemption and County Status Certificate

The Indiana county tax rules require precise tracking of employees' residence and work locations as of January 1st each year. CMiC’s payroll system ensures compliance with these regulations by:

-

Utilizing Exemption records in the PYTAXEXM table.

-

Relying on the Residence Location and Primary Work Location fields for accurate tax calculations.

-

Ensuring payroll administrators update Exemption records before each payroll run.

Tax Exemption Fields in CMiC

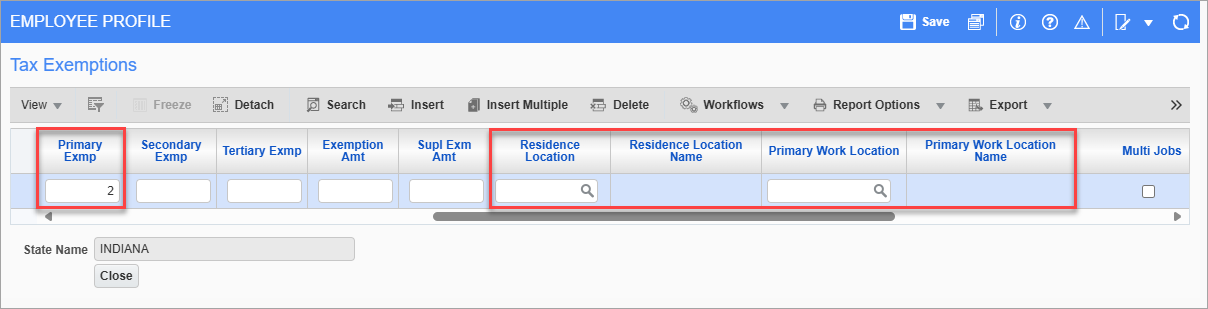

![Screenshot of Tax Exemptions pop-up launched from [Exemptions] button on Employee Profile.](../../../Resources/Images/PYU_12c_for_import/PYU_IndianaTax1.png)

Pop-up window launched from [Exemptions] button on Tax tab of Employee Profile screen

The Residence Location and Primary Work Location fields in the Tax Exemptions pop-up screen (PYTAXEXM) are used to accommodate Indiana's county tax rules. These fields determine the Indiana resident county tax or Indiana non-resident work county tax for the entire year. If an employee moves to a different county or state after January 1st, their county tax remains based on their status on January 1st.

NOTE: These fields are only enabled when "IN – Indiana" is selected in the State Code field and "All" is selected in the Work Location field in the Tax Exemptions screen.

For more information, please refer to [Exemptions] – Button.

Residence Location

This field is used to define the Indiana county where the employee resides as of January 1st.

Primary Work Location

This field is used to identify the Indiana county where the employee works as of January 1st.

Logic for Indiana County Tax Calculation

The system follows a hierarchical tax calculation process, where tax is applied based on the first condition that is satisfied.

-

Indiana Resident Tax Rule: If an employee lived in Indiana on January 1st, all earnings (including those earned outside Indiana) are subject to the resident county tax of their January 1st residence county.

-

Indiana Non-Resident Work County Tax Rule: If an employee worked in Indiana on January 1st, Indiana-based earnings are subject to the non-resident work county tax of their January 1st work location.

-

No Indiana County Tax: If neither of the above conditions is met, no Indiana county tax is calculated.

-

Exemption Record Requirement: The Indiana county tax rules apply only if an exemption record exists in the PYTAXEXM table with an effective date of January 1st or earlier. If no such record is found, the system defaults to the previous calculation method.

Implementation Guidelines for Payroll Administrators

Existing Employees with Indiana Exemptions

Employees with an Indiana Exemption record in CMiC must have their Residence and Work Location fields updated before the next payroll run.

Failure to specify these fields results in no county tax calculation.

New Employees or Those Without Indiana Exemptions

Employees gradually transitioned into the new method must have a valid Exemption record specifying their residence location and primary work location.

Once all employees have been updated, administrators should modify the Tax Type field from "Resident" to "Both" in the US Payroll - Payroll Tax Accounting screen. This ensures the non-resident work county tax is correctly calculated for those working in Indiana but residing outside the state.

Scenarios for Indiana County Tax Calculation

| Scenario | Tax Rule Applied |

|---|---|

| Employee lives and works in Indiana on January 1st. | Resident county tax applies to all earnings. |

|

Employee lives in Indiana on January 1st but works in another state. |

Resident county tax still applies. |

| Employee works in Indiana on January 1st but lives in another state. | Non-resident work county tax applies to Indiana earnings. |

| Employee moves to Indiana mid-year (either for work or residence). |

No county tax applies for the current year. If still in Indiana on January 1st of the following year, then Indiana county tax applies. |

Tax Calculation

The tax calculation follows these steps:

-

The system inserts an Exemption record with the following:

-

Number of State Exemptions

-

Residence Location

-

Primary Work Location

-

-

If the Residence Location and Primary Work Location fields are not specified the system will not have enough data to calculate the tax correctly.

Example: Employee with Two Indiana State Exemptions

An employee lives and works in Indiana and has two Indiana state exemptions. The following outcomes are possible:

-

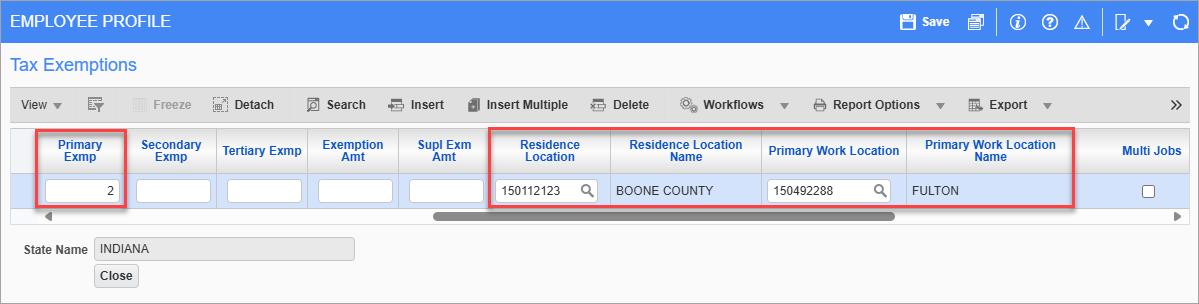

If the exemption fields are missing, the system defaults to the previous method, and no Indiana county tax is calculated. In the example below, the Residence Location and Primary Work Location fields are blank.

-

If the exemption fields are correctly populated, the Indiana county tax is applied based on the county tax rates. In the example below, the Residence Location and Primary Work Location fields are populated.

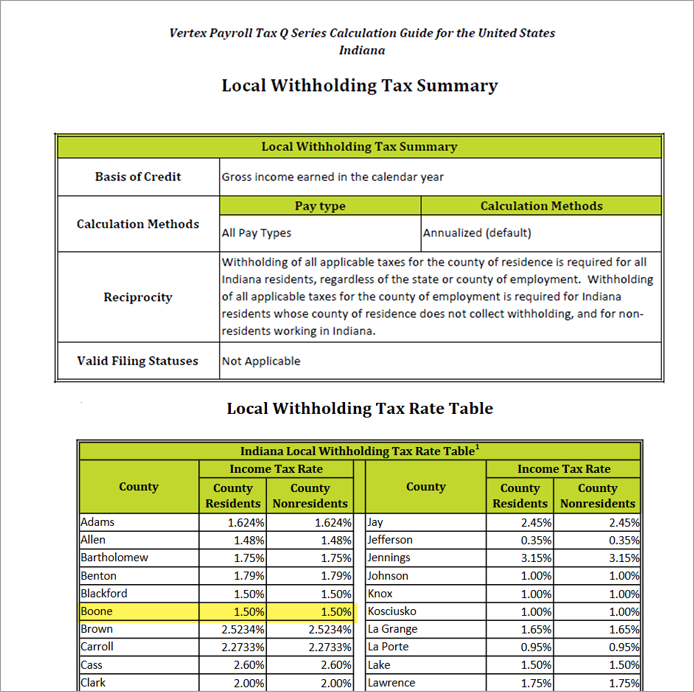

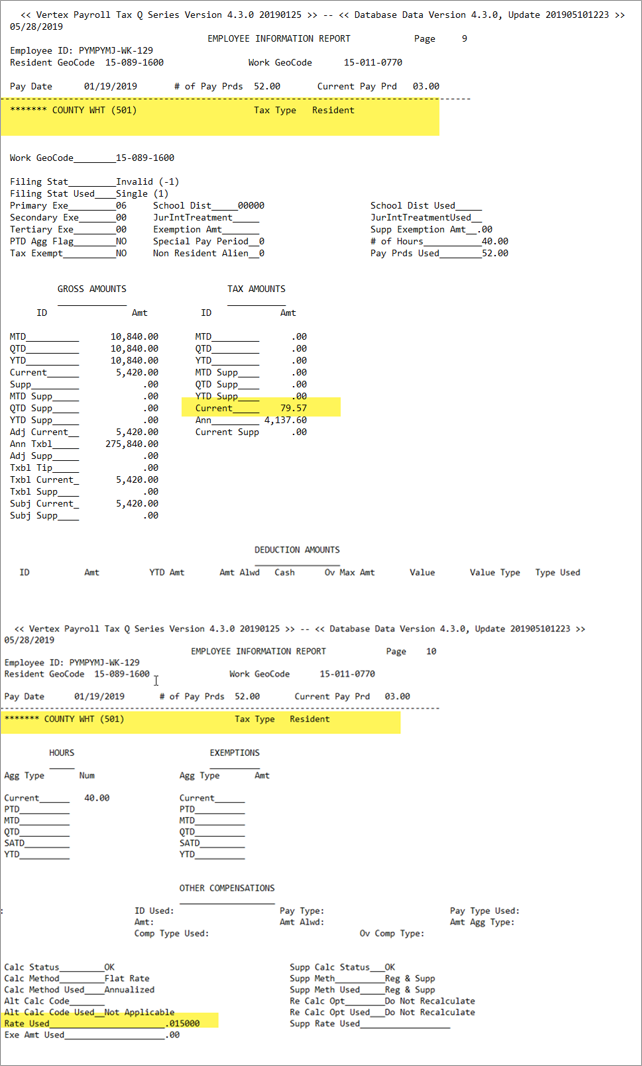

Sample Vertex reports:

Sample County Tax Rate

Sample Vertex Employee Information Report

Common Payroll Issues & Solutions

| Issue | Resolutions |

|---|---|

| Employee does not have an Indiana exemption record. | Ensure a valid PYTAXEXM record exists for January 1st or earlier. |

| Residence Location and Primary Work Location fields are missing. | Update these fields before payroll processing. |

| Employee moved to Indiana mid-year but is not taxed. | Taxes apply only if the employee was in Indiana on January 1st. |