Overview

Currently, when CMiC customers are upgrading from V10X Versions to R12, or when new customers are going live on R12 from their existing software, a plethora of concerns and questions around State Unemployment Insurance (SUI) calculation arise. The most frequently asked questions are, “Where should it be calculated?” or “Why is it not calculated in multiple states in a single pay period?”

In V10X or prior versions of CMiC software, CMiC adopted the SUI calculation which allows two methods. Firstly, if the employee works in more than one state then payroll calculates SUI for all states and secondly, credit is given to the most recent state if an employee moves to another state. However, this was an old method of calculating SUI before the new law and Vertex have adopted the NEW laws and have changed the SUI calculation.

Which State Gets the Taxes?

It can be challenging, at times, to determine the correct state to report and pay unemployment taxes for an employee who performs services in more than one state.

Reporting and paying unemployment taxes to the incorrect state can be time consuming.

The Federal Unemployment Tax Act (FUTA) provides guidelines for reporting unemployment wages involving an employee who performs services in more than one state during a calendar year.

NOTE: Unemployment wages must be reported to only one state.

All states were put into effect as regulated by the U.S. Department of Labor to determine the correct state to report an employee’s wages for state unemployment purposes.

Employers must review the following uniform set of four factors in chronological order. Accordingly, if the first set does not apply, the next set is reviewed until the facts and circumstances involving your employee demonstrate the state where the wages should be properly reported.

The four reporting factors (see below) are based on the facts and circumstances of each employee and employer, which may change frequently based on the industry and services provided.

When filing quarterly unemployment returns, employers should carefully review these four factors to determine where unemployment wages should be reported, and taxes paid for employees who perform services in multiple states.

See the links below for more detailed legislative laws around unemployment:

https://wdr.doleta.gov/directives/attach/UIPL20-04_AttachI.html

https://oui.doleta.gov/dmstree/uipl/uipl2k4/uipl_2004a1.htm

CMiC Solution to Multi-State SUI Calculation in R12

From the following uniform set of four factors, the employer can determine where the unemployment tax should be paid if an employee works in Multi-State.

-

Where the individual’s work is “localized.”

-

Where the “base of operations” is.

-

Where the place of direction or control is.

-

Where the employee’s place of residence is.

As per the XML-Interface, the unemployment tax must be calculated and reported to only one state.

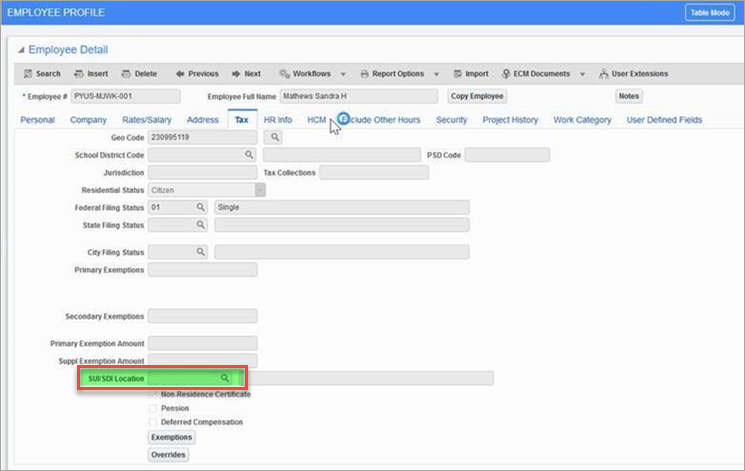

If a primary SUI location is specified, like our single SUI state on the Employee Profile, then it will calculate under that state. If no primary SUI location is specified, then it will pick one work location state from the XML work section.

Pgm: PYEMPLOY – Employee Profile; standard Treeview path: US Payroll > Setup > Employees > Employee Profile – Tax tab

Due to these legislative rules for determining where SUI is paid in Multi-State scenarios, the vertex XML-Interface has limitations and will calculate SUI only in a single state.

Therefore, employers must consider these four factors and define the state accordingly on the employee’s profile.